R&D Spending Allocation Trends

Strategy & Business conducted a study, Global Innovation 1000, of the top public companies spending the most on R&D to strengthen their brand from 2010 to 2015. The study found that while overall R&D spending is increasing, the total research and development allocation is shifting towards increased research and development of software offerings.

Why Shift Towards Software?

As software capabilities are rapidly developing there are increasing opportunities to develop product offerings to include additional features catering the demand for advanced services and technology. Popular examples of these developments include embedded software such as sensors and new features or network software connecting systems and communication between products, programs and people.

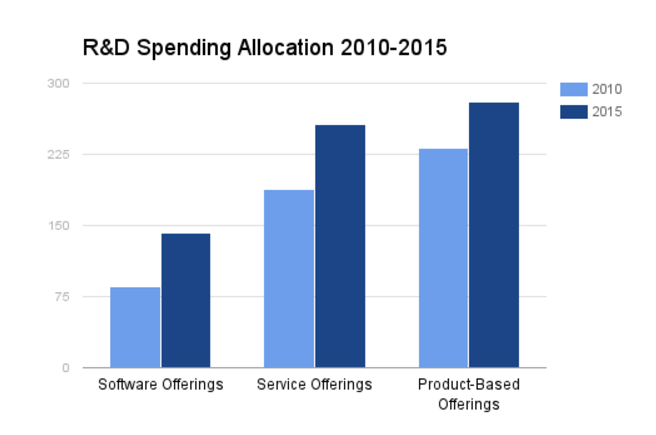

In analyzing the shift, a 34% rise in overall research and development spending was recorded at US$680 with a 65% increase in software R&D, a 36% rise in service R&D and a 21% rise in product-based R&D spending despite the fall of product-based in allocation share. This data is displayed in the chart. *Data from Strategy&Business Global Innovation 1000

Growth in software research and development is expected to continue engaging 77% of surveyed companies by 2020 from 30% in 2015. The study also concluded that companies investing larger percentages of R&D into software are growing at a higher rate than competitors investing less. Strategy & Business goes on to suggest that investment in software offerings appears to maintain company growth fairly independently of macroeconomic fluctuations assuring growth in successful R&D.

As supported by the research and development tax incentive, R&D spending as a whole is expected to continually increase. If you would like to discuss the R&D Tax Incentive further, please do not hesitate to contact one of Swanson Reed’s offices today.